The roots of the Protection & Indemnity Club or a P&I club were founded in 18th century England. Those were the days of sailing ships and extremely slow and inefficient communication system. Ship owners and the underwriters had limited contact and the hull insurance did not cover all aspects of loss on board. A group of ship owners formed an association to provide each other insurance cover. This association was a non-profit making body controlled by a group of close-knit ship owners. These associations were named as Mutual Hull Insurance Clubs. The basic principle of the club was that each member of the group of ship owners would share with other members the cost of any hull claim, which an individual member suffered. It was paid rate ably according to the value of the vessel or vessels owned by that member of the club. This spread the risk over a number of owners and provided the cover, which was otherwise lacking in the insurance market. Pooling of risks made the cover cheaper than what was available in the market. In addition, the club was able to have greater control over the handling of claims when compared to the insurance cover provided by underwriters. The increase in the volume and the complexities of world trade expanded the risks covered. In due course, the mutual insurance organisations joined forces to form the present date Protection and Indemnity Club. Most of the Protection & Indemnity Clubs were established by the beginning of 20th century. They were administered by a group of members, the committee, which met periodically to decide on the payment of claims and the levying of calls (premium).

Covers provided by the P and I club

Following are the typical covers provided by a P and I club:

- personal injury, claims to cover third party liabilities covering death or injury to crew, passenger and stevedores. etc.

- crew claims to cover repatriation

- collision liabilities

- fixed and floating objects claims

- cargo claims

- environmental pollution claims

- miscellaneous claims e.g. wreck removal, customs fines etc.

- freight, demurrage and defence for disputes under charter parties.

Claims other than above can also be considered under the so-called ‘Omnibus Rule’, in which the club committee has the discretion to consider deserving claims from any member at any time.

What is “call money” and how is decided by the P and I Club?

The premium rates to be paid to the club by a ship owner are called the “call money”. The amount is decided by the committee based on the fleet’s ship types, ages, gross tonnage, trades, flags, crew nationality, exposure to risks, and other factors including the member’s claims record and the likelihood of large claims in the coming year.

The member is advised of the total estimated call for the next 12 months; this comprises of an advance call and a supplementary call. Advance calls are levied on all members at the start of the P & I year, which is February 20th (on this date sailing vessels would depart for the Baltic from ports on the north-east coast of England following their winter lay-up and by tradition and still is the date from which insurance was required).

Later in the year, if claims have been heavier than expected, the managers will ask the members for a supplementary call to “balance the books”. Clubs aim to be accurate in their predictions of future claims so as not to burden owners with supplementary calls. Refunds are made when income (calls + investments) exceeds outgoing (claims + expenses).

Who are P&I club correspondents and what are their functions?

P & I clubs retain correspondents at numerous “ports worldwide. In the USA, a correspondent is normally a law firm with maritime lawyers. The correspondents:

Are for legal reasons, representatives and not agents of the club;

Will attend member vessels when so requested by the master or agent in order to protect a member’s interests;

Are generally well acquainted with the club’s rules and policy, etc.;

Will report any occurrence likely to result in claim on the club;

May, pending instructions, appoint surveyors to inspect damages;

Maybe instructed by the club “to offer letter of undertaking in case of possible liability. In most cases of bunkering oil pollution or damage to jetty etc., a bond is to be posted to avoid arrest.

Most clubs provide the ships with a list of correspondents.

How are claims of P& I clubs paid?

~Club LIMITS have been updated. Below for understanding purposes only~

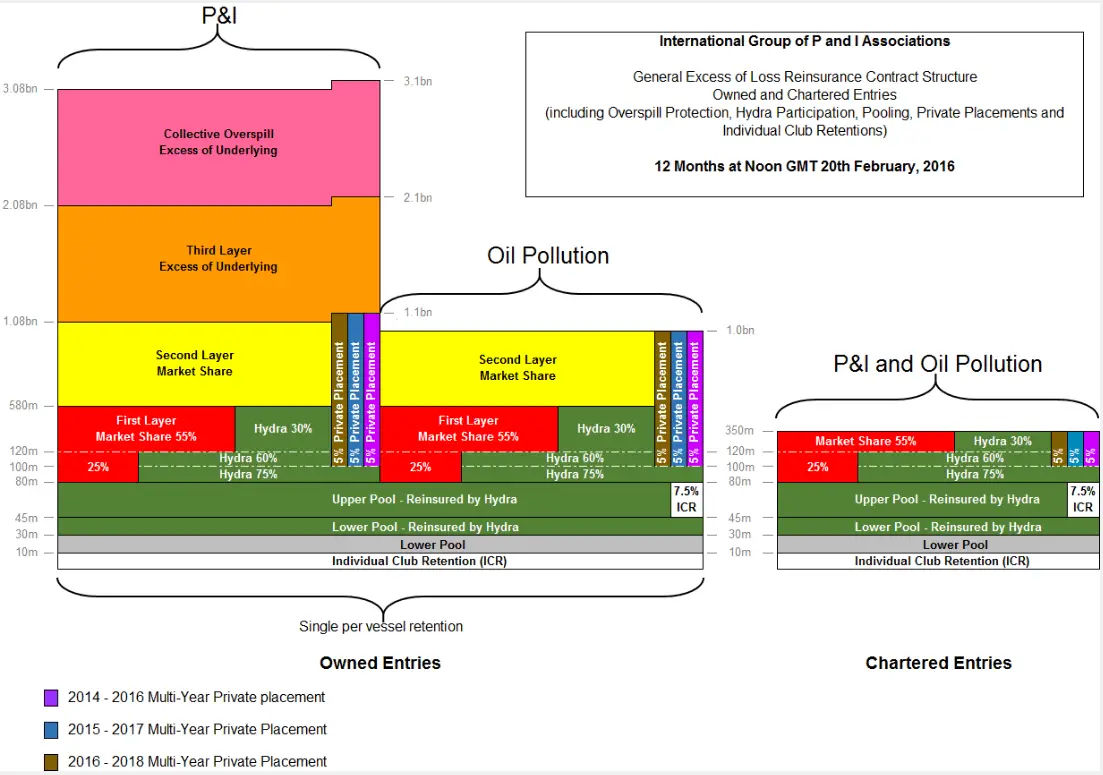

When a member of a P & I club has a claim, the first $5 million will be met by the club’s own fund. In excess of $5 million and up to $30 million the claim is divided among the member clubs in the International Group Pool (including the club making the claim), with the pooling contribution of each club being calculated taking into account its entered tonnage, premium income and claims record in the Pool. For claims in excess of the Pool limit, the International Group arranges an Excess of Loss reinsurance contract in the market; this currently provides cover for $2000 million ($2 billion) in excess of $30 million in relation to all types of claim except oil pollution, where the limit is $1000 million ($1 billion).

Should the claim ever exceed the upper limit of the Excess of Loss Contract, it should fall back on the Pool and be borne by each club pro rata according to its entered tonnage.

Such a claim is called an “overspill claim” and would be funded either from the club reserves or by making a special “overspill call” on the membership. For most of the history of die P & I clubs, there is no upper limit to cover, but there is an upper limit of $4.25 billion on overspill claims. Some clubs extensive reinsurance for overspill claims.

Updated Club Limits as of 2016/17

Club cover continues to contain a standalone cover limit for oil pollution of US $1 bn, a limit on passenger claims of US $2 bn, and a combined limit on passenger and crew claims of US $3 bn.

For 2016/17, the individual club retention has been increased from US $9 million to US $10 million, the previous upper and upper-upper pool layers have been merged into a single upper pool layer from US $45 million to US $80 million, and the GXL programme attachment remains at US $80 million. A further 5% multi-year US $ 1 billion (excess of US $100 million) private placement has been effected, and the Hydra coinsurance within the first GXL layer (US $500 million excess of US $80 million) has been slightly increased to include an additional 5% in the layer US $80 million-US $100 million.

Hydra is a segregated cell captive reinsurance company, established in Bermuda in 2005, through which the Group clubs collectively reinsure exposure in the lower and upper pool layers, and co-insure exposure in the first layer of the market GXL placement (US $80 million- US $580 million).

How does a ship owner register his claim?

A ship owner, who is a member of the club, must give immediate notification of any incident, which could result in a claim or liability within the scope of the club’s cover. Once a claim or a potential claim has been notified the club takes over the investigation and handling of the claim. It takes the help of the correspondents, surveyors and lawyers appointed by the club.

In liaison with the member, the club will handle the claim to its logical conclusion. If there is a third party claim where the member has to pay, the club will ask the member to pay for the liability. Once the member pays the amount, an indemnity (i.e. reimbursement) is asked for from the club in accordance with the club rules and the member’s terms of entry. The amount recoverable is subject to a deductible i.e. an amount agreed by the member to bear himself before he can claim from the club.

Which liabilities are normally not covered by the P & I clubs?

Clubs will not normally cover:

Ad valorem bill of lading

Deviation;

Delivery of cargo to a port other than the port specified in the bill of lading;

Failure to arrive or late arrival at a port of loading;

Delivery of cargo without production of bill of lading;

Ante-dated or post-dated bill of lading;

Clean bills of lading in case of damaged cargo;

Deck cargo carried on terms of an under-deck bill of lading;

Arrest or detention of an entered ship.

What are the P&I covers for pollution?

P & I cover for pollution liabilities is generally to the extent that the pollution is as a result of an escape or discharge or threatened escape or discharge of oil or any other substance. Clubs have traditionally covered:

- Liabilities for damages or compensation;

- Costs of reasonably-taken measures for preventing, minimizing or cleaning up pollution;

- Costs or liabilities incurred as a result of compliance with government directions during a pollution incident;

- Special compensation payable to salvers;

- Fines for pollution.

- AD VAleroum BIll pdf link

- Next

-

What is a Marine Policy? Basics you need to know!

DroppedThe Procedure For Transferring The Registry

Dropped

Admiring the hard work you put into your website and detailed information you present. It’s awesome to come across a blog every once in a while that isn’t the same outdated rehashed information. Great read! I’ve saved your site and I’m adding your RSS feeds to my Google account.

I really wanted to develop a small message so as to appreciate you for those lovely recommendations you are sharing on this website. My considerable internet investigation has finally been honored with really good concept to exchange with my co-workers. I ‘d admit that many of us website visitors actually are undoubtedly lucky to exist in a superb place with very many outstanding professionals with very helpful things. I feel very much happy to have encountered the site and look forward to tons of more fun times reading here. Thanks again for all the details.

I am also writing to let you know what a great experience our child developed visiting your web page. She realized a good number of issues, most notably how it is like to have an awesome coaching mindset to let many more with no trouble learn about certain multifaceted subject areas. You actually did more than people’s expectations. Thanks for coming up with the good, dependable, informative and in addition unique tips about the topic to Evelyn.

I am also commenting to make you understand what a excellent discovery my friend’s girl encountered reading through your site. She realized such a lot of things, which include what it’s like to have a great teaching character to have most people without problems fully understand selected tricky subject areas. You undoubtedly surpassed people’s desires. I appreciate you for offering these helpful, trusted, edifying and fun thoughts on this topic to Jane.

I must show my thanks to this writer just for rescuing me from such a problem. Right after looking throughout the the web and finding proposals that were not helpful, I believed my life was well over. Being alive without the solutions to the problems you have sorted out through your good site is a serious case, as well as those which could have in a wrong way affected my entire career if I had not come across the blog. The knowledge and kindness in dealing with all areas was excellent. I don’t know what I would’ve done if I had not come upon such a step like this. It’s possible to at this time look ahead to my future. Thanks very much for the reliable and result oriented help. I will not think twice to refer your site to any person who requires direction on this topic.

Needed to send you one very little remark just to thank you very much as before for all the pleasant thoughts you have provided above. It has been really unbelievably generous of people like you to make freely what a lot of folks could have offered for an e book to help with making some profit for themselves, certainly since you could have done it if you desired. Those pointers also worked like the easy way to understand that other people online have a similar fervor just like my personal own to know the truth somewhat more with regard to this matter. I think there are numerous more pleasurable times ahead for folks who look over your site.

I’m just writing to let you understand of the nice discovery my cousin’s girl found visiting the blog. She figured out so many details, which included what it’s like to have an excellent helping heart to make the rest clearly gain knowledge of various tricky subject areas. You undoubtedly did more than people’s expected results. I appreciate you for offering those warm and helpful, safe, explanatory and also fun tips about the topic to Mary.

I have to get across my gratitude for your kind-heartedness for those people that absolutely need help on this topic. Your very own commitment to passing the solution all over turned out to be rather good and has regularly permitted girls much like me to arrive at their aims. The warm and helpful guide can mean a great deal a person like me and much more to my office workers. Thanks a ton; from each one of us.

I wish to express appreciation to this writer just for bailing me out of such a difficulty. After searching through the world wide web and finding solutions which were not powerful, I figured my life was well over. Being alive without the strategies to the difficulties you’ve resolved by way of your good article is a critical case, as well as the ones that could have in a negative way affected my career if I had not encountered your blog. That mastery and kindness in dealing with all the stuff was important. I don’t know what I would’ve done if I hadn’t come across such a step like this. It’s possible to at this moment relish my future. Thank you so much for the professional and results-oriented guide. I will not think twice to endorse your blog post to any person who should have recommendations about this subject matter.

I not to mention my buddies were taking note of the best tips and hints on your website and then suddenly I had an awful suspicion I never expressed respect to the blog owner for those secrets. The people came certainly very interested to see all of them and have now undoubtedly been enjoying these things. Appreciate your simply being simply kind and for selecting variety of notable things most people are really wanting to be informed on. Our own sincere apologies for not expressing appreciation to earlier.

I would like to show thanks to this writer just for rescuing me from this particular challenge. Right after scouting throughout the the web and seeing principles that were not productive, I assumed my life was done. Being alive without the presence of solutions to the difficulties you’ve resolved all through your main site is a serious case, as well as the ones that would have in a wrong way affected my entire career if I hadn’t come across the website. Your good understanding and kindness in handling the whole lot was very useful. I don’t know what I would’ve done if I hadn’t discovered such a step like this. It’s possible to now look ahead to my future. Thanks for your time so much for your expert and effective help. I will not be reluctant to endorse the website to anyone who wants and needs care on this situation.

I needed to send you that bit of remark in order to say thanks again for those gorgeous guidelines you’ve featured on this site. This has been simply surprisingly open-handed with people like you to allow unhampered all that numerous people could possibly have offered for an e-book in making some money for themselves, primarily given that you could possibly have done it in case you wanted. Those advice as well worked as a great way to understand that other people have the same keenness like my own to know somewhat more in terms of this problem. I am certain there are lots of more enjoyable times in the future for people who looked at your blog post.

Needed to send you this very little word in order to thank you so much over again for your gorgeous basics you have documented at this time. It’s really incredibly open-handed of people like you to offer openly all that a few individuals would have offered for sale as an ebook to generate some dough for themselves, most importantly considering the fact that you could have done it if you ever wanted. Those tips as well acted to provide a fantastic way to understand that the rest have the same passion just like my personal own to know the truth more pertaining to this problem. I am certain there are a lot more fun situations up front for individuals who looked at your website.

My husband and i were very comfortable when Edward could do his researching because of the precious recommendations he gained from your very own web pages. It is now and again perplexing to simply continually be making a gift of instructions that some others may have been trying to sell. Therefore we grasp we have got the blog owner to give thanks to for that. The most important illustrations you made, the straightforward web site menu, the friendships you assist to promote – it is everything excellent, and it’s really making our son in addition to our family do think that situation is amusing, and that is extremely important. Many thanks for the whole thing!

I happen to be commenting to let you understand of the fabulous encounter my wife’s child went through viewing your web site. She discovered numerous issues, which include what it’s like to possess a marvelous teaching heart to have many more with no trouble understand various extremely tough issues. You truly exceeded our own expectations. Many thanks for producing such helpful, safe, explanatory and fun guidance on the topic to Jane.

I’m commenting to make you understand what a really good discovery my friend’s girl enjoyed using your blog. She came to find several issues, which include what it is like to possess an awesome giving mood to let certain people with no trouble learn about various tricky topics. You undoubtedly exceeded visitors’ expected results. Thanks for displaying the precious, safe, educational as well as fun guidance on this topic to Kate.

I must show appreciation to you for rescuing me from this type of setting. Right after surfing throughout the online world and meeting things which are not beneficial, I figured my entire life was gone. Being alive minus the strategies to the difficulties you’ve sorted out by means of your entire guide is a critical case, and ones which might have in a wrong way affected my entire career if I hadn’t noticed your web page. Your own personal skills and kindness in playing with every part was crucial. I am not sure what I would’ve done if I had not discovered such a point like this. I can at this point look forward to my future. Thanks very much for your professional and amazing help. I will not be reluctant to recommend the sites to any individual who should get assistance about this topic.

My husband and i were absolutely delighted when Louis could round up his inquiry via the ideas he made using your site. It’s not at all simplistic to just find yourself giving out concepts people have been trying to sell. We really see we’ve got the writer to give thanks to for that. Those explanations you’ve made, the straightforward website menu, the friendships you can help to foster – it’s got all fabulous, and it is assisting our son and the family feel that this topic is amusing, and that’s truly mandatory. Thank you for the whole thing!

I’m just writing to let you know of the awesome experience our child experienced reading through the blog. She picked up plenty of things, which include how it is like to possess an amazing giving spirit to get other people completely know just exactly various very confusing things. You undoubtedly exceeded readers’ desires. I appreciate you for producing these great, safe, explanatory and cool thoughts on that topic to Gloria.

My spouse and i ended up being quite delighted that John managed to carry out his inquiry through your precious recommendations he gained from your web page. It is now and again perplexing to simply happen to be handing out guidelines people today have been selling. And now we take into account we now have you to appreciate for this. All of the explanations you have made, the easy blog menu, the friendships you can assist to create – it is many unbelievable, and it’s assisting our son in addition to us reckon that this article is excellent, and that’s especially important. Many thanks for the whole thing!

Needed to send you this little bit of note to thank you again on the lovely information you’ve documented at this time. It was quite seriously generous with people like you to offer without restraint all a number of us could possibly have distributed for an e book to earn some dough on their own, specifically seeing that you could possibly have done it if you wanted. These creative ideas also worked to be a great way to comprehend other individuals have the same fervor really like mine to grasp a little more in terms of this condition. I know there are some more pleasurable moments in the future for individuals who start reading your blog post.

I wish to show my thanks to you just for rescuing me from such a predicament. After browsing throughout the search engines and coming across ways which were not pleasant, I assumed my life was well over. Living without the answers to the difficulties you’ve sorted out by way of the post is a crucial case, and the ones which could have badly affected my career if I hadn’t come across your website. Your own personal understanding and kindness in handling every aspect was tremendous. I am not sure what I would have done if I had not come upon such a point like this. I am able to at this point look forward to my future. Thanks a lot so much for this skilled and results-oriented guide. I will not think twice to refer the website to any person who should have guidance about this topic.

I wish to express some appreciation to this writer just for bailing me out of this particular condition. After exploring through the internet and seeing techniques that were not pleasant, I figured my life was done. Being alive without the answers to the problems you have sorted out as a result of your site is a serious case, and the ones which may have negatively damaged my career if I hadn’t discovered your site. Your own know-how and kindness in handling all the things was very helpful. I am not sure what I would have done if I hadn’t come across such a stuff like this. I’m able to at this moment look ahead to my future. Thanks a lot so much for this professional and results-oriented guide. I won’t hesitate to refer your blog to any person who would like guide on this topic.

I have to convey my appreciation for your kindness supporting people who should have guidance on your content. Your special commitment to passing the solution all around appears to be astonishingly helpful and has frequently allowed professionals just like me to attain their endeavors. Your personal invaluable publication means a great deal a person like me and substantially more to my peers. Thank you; from all of us.

I have to show some thanks to the writer just for rescuing me from this particular predicament. Because of exploring throughout the world-wide-web and coming across ways that were not powerful, I figured my life was well over. Living without the presence of approaches to the issues you have solved by way of your main review is a critical case, as well as the ones which might have in a wrong way damaged my career if I had not come across the blog. Your ability and kindness in taking care of almost everything was important. I am not sure what I would have done if I hadn’t discovered such a subject like this. I can also at this moment look ahead to my future. Thanks for your time very much for the expert and result oriented guide. I will not be reluctant to propose your web site to any individual who wants and needs guidelines about this issue.

I intended to create you a little bit of remark to be able to give many thanks over again considering the splendid secrets you’ve discussed on this site. This is quite tremendously open-handed of you to convey openly what most people would’ve marketed as an e book in order to make some dough for their own end, and in particular given that you could have done it if you ever wanted. The creative ideas additionally served to become a great way to comprehend most people have similar zeal just like mine to realize more and more in terms of this issue. I am sure there are some more enjoyable occasions in the future for people who read carefully your blog.

I am also writing to let you be aware of of the outstanding encounter my cousin’s princess enjoyed going through yuor web blog. She realized some things, which include what it’s like to have an awesome teaching mindset to have certain people completely completely grasp a variety of specialized subject areas. You really did more than visitors’ desires. I appreciate you for presenting those great, safe, explanatory and as well as cool guidance on that topic to Lizeth.

I simply had to thank you so much again. I do not know the things that I could possibly have accomplished without the actual concepts contributed by you about this subject matter. It was before a very fearsome circumstance in my circumstances, nevertheless looking at your specialized approach you dealt with it forced me to leap for joy. Now i am happier for this assistance and then wish you realize what a powerful job you happen to be getting into educating people thru a blog. I am sure you haven’t got to know all of us.

My wife and i ended up being glad when Chris could do his inquiry through the entire precious recommendations he gained out of your site. It’s not at all simplistic to simply continually be giving out procedures many people may have been trying to sell. So we take into account we have the website owner to thank for that. These illustrations you have made, the simple web site menu, the relationships you help foster – it’s got many remarkable, and it’s really helping our son and the family feel that this topic is thrilling, which is certainly really important. Thank you for the whole thing!

I want to voice my respect for your kind-heartedness supporting men who absolutely need assistance with this one subject matter. Your real dedication to passing the solution across appeared to be particularly advantageous and has continually encouraged guys and women like me to get to their dreams. The interesting instruction means much to me and additionally to my office colleagues. With thanks; from each one of us.

I’m just writing to let you be aware of of the really good discovery my cousin’s child encountered browsing your blog. She picked up a wide variety of details, with the inclusion of how it is like to have a marvelous giving heart to make the rest very easily know precisely specified complicated topics. You actually exceeded our own desires. I appreciate you for distributing these warm and friendly, trustworthy, informative and even fun thoughts on your topic to Sandra.

My wife and i got absolutely peaceful that Louis could finish off his inquiry through the entire ideas he made out of your web site. It is now and again perplexing to simply be freely giving tips that the rest might have been making money from. We really already know we have got you to thank because of that. The specific illustrations you made, the easy web site menu, the relationships your site aid to engender – it’s all superb, and it’s letting our son in addition to us do think the subject is enjoyable, which is extraordinarily indispensable. Thanks for everything!

I really wanted to jot down a small comment to appreciate you for these amazing information you are giving at this website. My long internet look up has at the end of the day been rewarded with pleasant suggestions to go over with my close friends. I would suppose that we site visitors actually are truly endowed to exist in a fabulous place with many special professionals with interesting secrets. I feel very lucky to have used your web pages and look forward to tons of more amazing moments reading here. Thank you once again for everything.

My spouse and i have been now satisfied when Michael managed to carry out his investigation from your ideas he gained from your very own web pages. It is now and again perplexing just to choose to be giving away tips and hints which usually people today have been selling. We keep in mind we have got the writer to thank for that. The entire illustrations you’ve made, the simple blog navigation, the friendships you will help to create – it’s got everything sensational, and it’s really leading our son in addition to us believe that this concept is amusing, and that’s pretty serious. Many thanks for everything!

I wanted to make a small word so as to say thanks to you for the splendid ideas you are sharing here. My long internet research has at the end been recognized with good facts and strategies to talk about with my company. I would repeat that we readers actually are really lucky to be in a remarkable website with many perfect individuals with beneficial tips and hints. I feel pretty privileged to have discovered your entire web page and look forward to really more brilliant minutes reading here. Thank you again for all the details.

I precisely needed to thank you so much once again. I do not know the things that I could possibly have tried without the type of smart ideas documented by you on such a subject matter. Certainly was an absolute difficult circumstance in my position, nevertheless seeing the specialized technique you handled it made me to leap with gladness. I will be happier for the guidance and trust you are aware of an amazing job you’re doing instructing the mediocre ones via a blog. More than likely you have never encountered all of us.

Thanks a lot for giving everyone an extremely superb possiblity to check tips from this site. It is often very ideal and full of amusement for me and my office mates to search your website at a minimum 3 times per week to study the newest things you will have. And definitely, I’m also actually motivated with your superb things you give. Some 4 ideas in this posting are in reality the very best we have all ever had.

I would like to show some thanks to the writer just for rescuing me from such a issue. Right after surfing around throughout the the net and coming across thoughts which are not productive, I thought my life was well over. Being alive without the presence of approaches to the issues you’ve resolved by way of your good article is a critical case, and those that would have in a wrong way damaged my entire career if I had not discovered your web blog. Your good know-how and kindness in dealing with a lot of stuff was valuable. I don’t know what I would have done if I hadn’t come upon such a step like this. I can also at this moment look ahead to my future. Thanks a lot very much for your specialized and amazing guide. I won’t think twice to suggest your blog to any individual who should receive counselling about this matter.

I precisely desired to thank you so much again. I’m not certain the things that I might have implemented in the absence of those hints revealed by you about this topic. It previously was a very challenging matter for me, however , viewing the very skilled form you treated that made me to weep for joy. Extremely grateful for this advice and in addition trust you know what a powerful job you were carrying out training the mediocre ones via your website. More than likely you have never encountered all of us.

My wife and i felt now contented that Chris managed to finish off his research through your ideas he acquired through the weblog. It’s not at all simplistic to just possibly be giving out instructions which usually some other people could have been trying to sell. So we already know we now have you to give thanks to because of that. Those illustrations you made, the straightforward blog navigation, the friendships you make it easier to foster – it is mostly fantastic, and it’s leading our son and our family believe that that content is entertaining, and that is extremely essential. Many thanks for all the pieces!

I not to mention my pals ended up checking the nice recommendations found on your site while quickly I got an awful suspicion I never expressed respect to the site owner for those techniques. Those young men had been consequently joyful to read them and have now sincerely been having fun with those things. Appreciation for actually being well kind as well as for selecting this form of important information millions of individuals are really desperate to discover. My honest apologies for not expressing appreciation to you earlier.

https://christianegossel.org/apps/blog/show/45520616-2009-collection-of-moments?siteId=137494839&locale=en-US&fw_comments_page=335&fw_comments_order=DESC&siteId=137494839&locale=en-US

https://www.sherberandrad.com/pages/face-cosmetic-surgery-face-lift-overview

http://www.digitalnewszone.com/6006/why-purchase-wein-online-instead-of-local-retailers.html

https://meiguo.com/read-1371791-1.html

https://anime.myreviewer.com/Article/162760/New-iSAW-EXtreme

http://aesthetic-websites.sandbox.webvalley.cz/blog/2023/03/13/in-den-meisten-fallen-seien-manner-die-initiatoren/

https://talentspots.be/apps/blog/show/prev?from_id=45618639&fw_comments_page=80&fw_comments_order=DESC&siteId=137065384&locale=nl-be

https://top10r.ru/iskusstvo-arhitektura/240-top-10-samye-neobychnye-restorany-mira.html

http://www.lignum.vsi.ru/index.php?nma=contacts&fla=index

Thanks for finally talking about > What is a P&I club?

– What I stand for < Loved it!

http://homemoneysavingtips.com/2022/10/30/how-to-save-money-when-trying-to-stay-warm-press-herald/

Hello my family member! I want to say that this post is awesome,

nice written and come with approximately all significant infos.

I would like to see more posts like this .

http://www.mindreading.jp/blog/archives/200810/2008-10-16T0846.html

http://echogreentrading.com/message/index.php?class1=52&page=215

There is noticeably a bundle to find out about this. I assume you made certain good factors in features also.

https://chaek.ru/imperatorskiy-farfor/kobaltovaya-setka/koltso-dlya-salfetok-farforovoe-forma-molodezhnaya-risunok-kobaltovaya-setka-imperatorskiy-farforovyy-zavod/reviews/

https://backporchproduce.com/apps/blog/show/prev?from_id=49807433&siteId=141277944&locale=en-US&fw_comments_page=6&fw_comments_order=ASC&siteId=141277944&locale=en-US

http://www.ftftftf.com/zzz_NotInUse/zzzz_bbslb/light.cgi/www.ravimotorcycles.com/yxjvJwlNbVkchyhQZZ

http://www.seirpardazaniran.com/fa/index.php/en/category/item/404-2017-09-03-09-57-53/404-2017-09-03-09-57-53?start=108

fenofibrate usa buy cheap fenofibrate fenofibrate drug

Youre so cool! I dont suppose Ive learn something like this before. So good to find anyone with some authentic ideas on this subject. realy thank you for starting this up. this website is one thing that is wanted on the net, somebody with a little originality. helpful job for bringing one thing new to the internet!

http://wool4build.eu/index.php/component/k2/item/31-trade

hello there and thank you for your info – I’ve certainly picked up something new from right here.

I did however expertise some technical points using this site, as I experienced to reload the web site a

lot of times previous to I could get it to load correctly. I had been wondering if your hosting is OK?

Not that I’m complaining, but slow loading instances times will very frequently affect your placement in google and can damage your high-quality score if advertising and marketing with Adwords.

Anyway I’m adding this RSS to my e-mail and can look out for much more

of your respective interesting content. Make sure you update this again very soon.

Youre so cool! I dont suppose Ive read anything like this before. So nice to find somebody with some unique ideas on this subject. realy thanks for starting this up. this web site is something that is wanted on the internet, somebody with just a little originality. useful job for bringing one thing new to the internet!

I do not even understand how I stopped up here,

but I believed this post was once great. I do not know

who you’re but definitely you are going to a well-known blogger if you happen to aren’t already.

Cheers!

I really like it when individuals get together and share ideas.

Great site, keep it up!

WOW just what I was looking for. Came here by searching for Plumber

Good post. I learn one thing more challenging on totally different blogs everyday. It’ll all the time be stimulating to learn content material from different writers and apply just a little something from their store. I抎 choose to make use of some with the content on my blog whether you don抰 mind. Natually I抣l give you a hyperlink on your net blog. Thanks for sharing.

This actually answered my drawback, thanks!

I couldn’t refrain from commenting. Perfectly written!

Hi! I’ve been following your web site for a while now and finally

got the courage to go ahead and give you a shout out from Lubbock

Tx! Just wanted to mention keep up the good work!

Greetings! This is my first comment here so I just wanted to give a quick shout out and say I genuinely enjoy reading through your blog posts.

Can you recommend any other blogs/websites/forums that go over

the same subjects? Thanks for your time!

Fabulous, what a webpage it is! This webpage presents helpful data to

us, keep it up.

Do you mind if I quote a few of your articles as long as I

provide credit and sources back to your weblog?

My blog site is in the very same niche as yours and my

users would truly benefit from a lot of the information you present here.

Please let me know if this ok with you. Cheers!

Do you mind if I quote a few of your posts as long as

I provide credit and sources back to your weblog? My blog is in the very same area of interest as yours and my users would truly benefit from some of

the information you present here. Please let me know if this alright with

you. Thanks!

Greetings I am so glad I found your webpage, I really found you by accident, while I was researching on Yahoo for something else, Regardless I am here now and would just like to say thank you for a fantastic post and

a all round exciting blog (I also love the theme/design), I don’t have time to read through it all at the minute but I have

bookmarked it and also included your RSS feeds, so when I have

time I will be back to read a great deal more, Please do

keep up the superb jo.

Howdy just wanted to give you a quick heads up.

The words in your post seem to be running off the screen in Ie.

I’m not sure if this is a format issue or something to do with web browser compatibility

but I figured I’d post to let you know. The layout look great though!

Hope you get the issue solved soon. Many thanks

I read this post completely about the resemblance

of most up-to-date and previous technologies, it’s amazing article.

Hi are using WordPress for your blog platform? I’m new to the

blog world but I’m trying to get started and set up my own. Do you

need any html coding expertise to make your own blog?

Any help would be really appreciated!

Good day! Would you mind if I share your blog with my

myspace group? There’s a lot of people that I think would really enjoy your content.

Please let me know. Cheers

It’s impressive that you are getting ideas from this article as well

as from our argument made at this place.

Do you have any video of that? I’d want to find out more details.

Oh my goodness! Incredible article dude! Thank you so much, However I am having

issues with your RSS. I don’t know the reason why I can’t join it.

Is there anybody having similar RSS issues? Anybody

who knows the answer can you kindly respond?

Thanks!!

I’ve been browsing online more than 4 hours today, yet I never found any interesting article like yours.

It is pretty worth enough for me. In my view, if all webmasters and bloggers made good content as you did, the web will be much more useful than ever before.

I’ll right away clutch your rss as I can’t find your email subscription link or newsletter service.

Do you’ve any? Kindly permit me recognise in order

that I could subscribe. Thanks.

Howdy! I could have sworn I’ve been to this site before but after browsing through some of the post

I realized it’s new to me. Anyhow, I’m definitely delighted I found it and I’ll be book-marking and

checking back often!

Actually no matter if someone doesn’t know afterward its up to other people that they will assist, so here it occurs.

A powerful share, I simply given this onto a colleague who was doing a little evaluation on this. And he actually purchased me breakfast as a result of I found it for him.. smile. So let me reword that: Thnx for the treat! However yeah Thnkx for spending the time to discuss this, I feel strongly about it and love reading extra on this topic. If attainable, as you become expertise, would you mind updating your weblog with extra details? It’s highly useful for me. Large thumb up for this weblog submit!

Attractive portion of content. I simply stumbled upon your site and in accession capital to say that

I get in fact enjoyed account your blog posts. Any way I’ll be subscribing to your augment or even I success you get entry to

persistently rapidly.

I enjoy what you guys are up too. Such clever work and coverage!

Keep up the superb works guys I’ve added you guys to my blogroll.

Right now it seems like Drupal is the top blogging platform available right now.

(from what I’ve read) Is that what you are using on your

blog?

You can definitely see your skills in the article you write.

The sector hopes for more passionate writers such as

you who are not afraid to mention how they believe.

All the time follow your heart.

Hi there! This article could not be written much better!

Looking through this post reminds me of my previous roommate!

He always kept talking about this. I will forward this article to

him. Fairly certain he’ll have a very good read. I

appreciate you for sharing!

There are some fascinating closing dates on this article however I don抰 know if I see all of them center to heart. There may be some validity however I’ll take maintain opinion until I look into it further. Good article , thanks and we wish extra! Added to FeedBurner as well

Post writing is also a excitement, if you know after

that you can write if not it is complex to write.

I know this website presents quality depending articles or reviews

and other material, is there any other site which provides these

stuff in quality?

My relatives all the time say that I am killing my time here at net, except I

know I am getting familiarity all the time by reading such nice articles

or reviews.

WONDERFUL Post.thanks for share..extra wait .. ?

It’s perfect time to make some plans for the future and it is time to be happy.

I’ve read this put up and if I could I wish to

counsel you some interesting issues or tips.

Maybe you can write next articles regarding this article.

I wish to read even more issues about it!

You actually make it seem so easy with your presentation but I find

this matter to be really something that I think I

would never understand. It seems too complex and extremely broad for

me. I am looking forward for your next post, I will try to get the hang of it!

I think this is among the most important information for

me. And i am glad reading your article. But should remark on few general things, The website

style is wonderful, the articles is really excellent : D.

Good job, cheers

Hi there, all the time i used to check web site posts here early in the break of day,

because i like to find out more and more.

female cialis tadalafil sildenafil 100mg pills for men viagra 100mg sale

Once I originally commented I clicked the -Notify me when new feedback are added- checkbox and now every time a comment is added I get four emails with the identical comment. Is there any method you possibly can remove me from that service? Thanks!

how to get zaditor without a prescription purchase tofranil sale imipramine 25mg generic

buy minoxytop solution cialis for daily use best ed drug

order acarbose 25mg online buy fulvicin 250mg brand griseofulvin

order aspirin 75 mg generic cost levoflox 500mg imiquimod generic

dipyridamole ca lopid 300 mg for sale buy pravastatin 20mg without prescription

order melatonin for sale danazol ca danazol drug

buy cheap generic duphaston buy generic duphaston for sale purchase jardiance for sale

purchase fludrocortisone sale florinef 100 mcg uk imodium 2mg ca

It’s hard to come by experienced people about this topic, but you sound like you know what you’re

talking about! Thanks

Appreciate this post. Let me try it out.

There is definately a great deal to find out about this subject.

I really like all of the points you have made.

buy prasugrel 10mg online cheap prasugrel 10mg tablet order detrol for sale

order monograph mebeverine tablet buy pletal pills for sale

order generic ferrous 100 mg sotalol 40mg uk sotalol 40mg generic

buy mestinon 60 mg sale rizatriptan 10mg for sale rizatriptan sale

Do you mind if I quote a couple of your articles as

long as I provide credit and sources back to your site?

My blog site is in the very same area of

interest as yours and my users would really benefit from some of the information you present here.

Please let me know if this ok with you. Thank you!

all the time i used to read smaller articles which also clear their motive, and that is also happening with this article

which I am reading now.

vasotec canada order bicalutamide generic buy generic lactulose over the counter

xalatan price buy rivastigmine purchase exelon pills

premarin canada buy cabergoline pills buy viagra 50mg without prescription

buy prilosec 20mg pill oral metoprolol 100mg buy metoprolol generic

order micardis sale micardis 20mg canada molnunat 200 mg pills

buy cialis 10mg pill usa viagra sales buy viagra 100mg online cheap

generic cenforce 100mg cenforce 50mg usa order chloroquine

modafinil 200mg pill phenergan brand buy deltasone 40mg online

buy cefdinir generic purchase lansoprazole pills prevacid cost

buy accutane 20mg pill buy zithromax cheap buy zithromax online

order azipro pill cheap gabapentin sale where can i buy neurontin

buy cheap generic atorvastatin purchase proventil generic oral norvasc 10mg

free spins no deposit canada real money spins furosemide 100mg without prescription

pantoprazole 20mg usa buy pantoprazole pills order phenazopyridine 200mg online cheap

gambling addiction casinos online ivermectin 3mg dose

symmetrel over the counter cheap symmetrel purchase dapsone sale

buy generic clomid over the counter generic imdur 40mg buy imuran 50mg generic

buy medrol cheap order generic adalat 30mg buy generic triamcinolone for sale

levitra 20mg ca buy tizanidine no prescription tizanidine online order

cheap coversyl oral clarinex buy allegra 180mg online cheap

buy phenytoin 100 mg online cheap order phenytoin pills order ditropan 5mg pills

buy ozobax online cheap buy endep buy ketorolac for sale

cheap claritin buy loratadine sale dapoxetine 30mg tablet

order baclofen sale buy ketorolac sale purchase toradol

buy alendronate generic cost macrodantin 100mg macrodantin 100 mg brand

inderal 20mg cost buy motrin 600mg generic buy plavix cheap

purchase glimepiride without prescription order amaryl 4mg sale etoricoxib ca

pamelor 25 mg brand nortriptyline 25 mg tablet generic paracetamol 500 mg

coumadin 2mg pill paroxetine where to buy where to buy metoclopramide without a prescription

buy orlistat online cheap order asacol 400mg online purchase diltiazem pills

pepcid 20mg sale tacrolimus 5mg us brand prograf 1mg

azelastine 10ml ca zovirax 800mg pill cheap avapro 150mg

buy nexium online cheap cheap esomeprazole 40mg buy cheap generic topiramate

allopurinol oral generic allopurinol 100mg crestor sale

sumatriptan 50mg brand dutasteride pill dutasteride order

buspirone 5mg brand cordarone for sale cordarone us

zantac 150mg over the counter order mobic 7.5mg sale buy generic celebrex

motilium 10mg sale sumycin 500mg drug tetracycline 250mg over the counter

buy flomax 0.4mg generic buy zocor 20mg generic buy simvastatin 10mg pill

buy aldactone for sale propecia pill cheap propecia 5mg

help write my paper academic writers online where can i buy an essay

purchase fluconazole generic ciprofloxacin for sale online buy cipro 500mg generic

order aurogra 50mg generic brand estrace 1mg oral yasmin

buy metronidazole 400mg generic sulfamethoxazole tablet order keflex 500mg

generic lamotrigine 50mg oral lamictal 50mg purchase vermox pill

buy generic clindamycin for sale cleocin 300mg us order fildena 50mg for sale

purchase retin generic order avanafil 100mg without prescription buy avanafil without a prescription

order nolvadex 20mg pill order tamoxifen 20mg pill symbicort canada

tadacip where to buy voltaren 50mg over the counter order indomethacin 75mg without prescription

order axetil pill buy ceftin 500mg pills order robaxin 500mg pills

where to buy trazodone without a prescription clindamycin order clindac a generic

lamisil 250mg cheap gambling online win real money best no deposit free spins

buy aspirin generic top 5 real money casinos online casinos for real money

help with assignments uk colleges without essays cefixime 200mg price

help writing papers for college casino games real money gambling addiction

trimox cost biaxin 500mg cheap buy clarithromycin paypal

buy generic calcitriol 0.25 mg order trandate 100mg sale fenofibrate 160mg uk

clonidine 0.1mg brand antivert brand buy spiriva 9mcg generic

best teen acne treatment products buy trileptal pills for sale buy oxcarbazepine pills for sale

minocycline pills order ropinirole for sale requip cheap

alfuzosin tablet treat heartburn without antacids medication that reduces stomach acid

buy letrozole online buy albenza 400mg without prescription abilify 30mg price

doctor sleep online free oral medication for thinning hair 100 guaranteed weight loss pills

cymbalta 20mg uk modafinil over the counter provigil price

otc medication for stomach ulcer ventricular tachycardia medication list different types of urinary infections

generic phenergan stromectol 3mg usa ivermectin 12mg for humans

get contraceptive pill online birth control cost without insurance medication for premature ejaculation

order deltasone 40mg without prescription amoxil 250mg brand amoxil 250mg canada

medicine for ulcer liquid medication thats makes you puke medication to make you fart

buy generic azithromycin online gabapentin for sale online purchase neurontin online

buy generic urso over the counter ursodiol us zyrtec price

order strattera 10mg online cheap strattera 10mg cheap order generic zoloft

lasix 100mg pill buy generic ventolin for sale ventolin 2mg drug

buy lexapro without prescription prozac 40mg sale order generic revia 50 mg

where can i buy combivent ipratropium 100mcg generic zyvox 600mg tablet

augmentin 1000mg price augmentin oral buy clomid 50mg online cheap

buy nateglinide medication buy generic starlix online order generic candesartan 16mg

vardenafil cost buy cheap tizanidine order hydroxychloroquine 200mg online

order tegretol generic buy ciplox no prescription generic lincocin 500mg

cenforce uk buy aralen 250mg without prescription glycomet 1000mg cheap

lipitor for sale online prinivil us buy zestril 2.5mg online cheap

order duricef generic buy combivir pill lamivudine online order

buy cabergoline online cheap buy dostinex generic priligy 90mg over the counter

depo-medrol us oral aristocort buy generic clarinex online

buy cytotec sale misoprostol us brand diltiazem

nootropil us betnovate 20 gm generic generic clomipramine

zovirax 800mg canada crestor 10mg usa crestor over the counter

buy sporanox 100 mg online brand progesterone tinidazole 300mg pill

ezetimibe 10mg tablet buy domperidone generic buy sumycin 500mg generic

cheap zyprexa 10mg bystolic brand order diovan 80mg online

how to buy cyclobenzaprine cyclobenzaprine 15mg tablet buy ketorolac generic

order generic colcrys order clopidogrel 75mg pill methotrexate online

progesterone only pill for acne benzoyl peroxide canada topical acne medication prescription list

do you need a prescription order astelin 10 ml nasal spray best non prescription allergy medication

Joyful, I’ve ascended to this new height with this riveting book, many thanks to the author!

Happy New Year, everyone!

Well-done article! If you’re looking for a writer, I’m ready and eager to help

latest on heartburn medication buy rulide online cheap

Impressive writing! Some added visual content could make it even more appealing. Check out my website for potential resources.

Excellent narrative! Including more visuals could really elevate the content. My website may have the resources you need.

This piece was a true eye-opener! I’m eager to write for your blog.

online doctors who prescribe zolpidem meloset 3mg drug

buy deltasone 5mg generic buy prednisone 10mg online cheap

Saya suka struktur argumen Anda. Sangat meyakinkan.

vomiting after you take medication best pain relief for pancreatitis

Is the author still active on the blog? We need more posts on this subject!

Excellent article! The insights provided are valuable, and I think adding more images in your future articles could make them even more compelling. Have you considered that?

Bravo on the article! 👍 The insights are well-expressed, and I believe incorporating more images in your next articles could be beneficial. Have you thought about that? 🖼️

Oh my goodness! Incredible article dude! Thanks, However I am encountering

troubles with your RSS. I don’t know the reason why I can’t subscribe to it.

Is there anybody else having similar RSS problems? Anybody who knows

the solution will you kindly respond? Thanx!!

prescription meds for acne teenagers crotamiton online order antibiotics for pimple pills

Terrific text, a recommended exploration!

Artikel ini luar biasa! Cara klarifikasinya sungguh memikat dan sangat mudah untuk dipahami. Sudah nyata bahwa telah banyak usaha dan penelitian yang dilakukan, yang sungguh mengesankan. Penulis berhasil membuat subjek ini tidak hanya menarik tetapi juga seru untuk dibaca. Saya dengan semangat menantikan untuk menjelajahi konten seperti ini di masa depan. Terima kasih atas berkontribusi, Anda melakukan pekerjaan yang hebat!

🚀 Wow, blog ini seperti petualangan fantastis melayang ke galaksi dari kegembiraan! 💫 Konten yang menarik di sini adalah perjalanan rollercoaster yang mendebarkan bagi imajinasi, memicu ketertarikan setiap saat. 🌟 Baik itu gayahidup, blog ini adalah harta karun wawasan yang menarik! #PetualanganMenanti Berangkat ke dalam perjalanan kosmik ini dari pengetahuan dan biarkan imajinasi Anda melayang! 🚀 Jangan hanya mengeksplorasi, alami sensasi ini! #BahanBakarPikiran 🚀 akan bersyukur untuk perjalanan menyenangkan ini melalui ranah keajaiban yang tak berujung! 🚀

prescribed medication for stomach pain cost lamivudine 100 mg

purchase absorica generic order accutane pills order isotretinoin 10mg pills

virtual visit online physician insomnia pill meloset 3 mg

amoxil medication generic amoxicillin 250mg buy amoxil 500mg generic

zithromax 250mg usa buy zithromax 250mg generic azithromycin price

cheap neurontin pill neurontin 600mg drug

purchase azipro for sale buy azipro 250mg online cheap azipro buy online

purchase lasix generic buy generic furosemide

prednisolone buy online omnacortil 40mg drug omnacortil online order

amoxicillin 500mg usa amoxil 1000mg ca order amoxicillin 1000mg for sale

buy doxycycline 200mg pill buy doxycycline 100mg for sale

buy albuterol 2mg pill albuterol inhalator us buy albuterol inhalator without prescription

purchase amoxiclav without prescription buy augmentin pills for sale

serophene brand buy clomid 50mg online cheap cheap serophene

After exploring a handful of the blog articles on your website,

I really like your technique of writing

a blog. I book-marked it to my bookmark webpage list and will be checking

back soon. Take a look at my website too and tell me how

you feel.

cheap tizanidine 2mg tizanidine generic buy generic tizanidine online

buy generic rybelsus online cost semaglutide 14mg rybelsus over the counter

prednisone 10mg us prednisone 10mg over the counter deltasone over the counter

brand rybelsus semaglutide cost generic rybelsus

accutane brand where to buy isotretinoin without a prescription order accutane 40mg online cheap

albuterol buy online buy albuterol 2mg online buy ventolin 4mg online cheap

amoxil 1000mg canada amoxicillin 1000mg for sale amoxil for sale

cheap augmentin 375mg order generic augmentin 1000mg buy generic augmentin 1000mg

buy generic azithromycin 250mg order zithromax 250mg online cheap buy zithromax no prescription

💫 Wow, this blog is like a cosmic journey blasting off into the galaxy of wonder! 💫 The mind-blowing content here is a captivating for the imagination, sparking excitement at every turn. 🌟 Whether it’s lifestyle, this blog is a treasure trove of exciting insights! 🌟 🚀 into this exciting adventure of discovery and let your imagination soar! 🚀 Don’t just explore, experience the excitement! 🌈 🚀 will be grateful for this exciting journey through the dimensions of endless wonder! 🌍

🚀 Wow, this blog is like a rocket blasting off into the universe of endless possibilities! 💫 The thrilling content here is a captivating for the imagination, sparking curiosity at every turn. 🌟 Whether it’s lifestyle, this blog is a treasure trove of exhilarating insights! 🌟 Dive into this thrilling experience of imagination and let your imagination roam! ✨ Don’t just read, experience the thrill! #BeyondTheOrdinary Your mind will be grateful for this exciting journey through the worlds of awe! ✨

🌌 Wow, this blog is like a cosmic journey blasting off into the galaxy of endless possibilities! 🌌 The mind-blowing content here is a thrilling for the imagination, sparking curiosity at every turn. 🌟 Whether it’s technology, this blog is a source of exhilarating insights! #InfinitePossibilities 🚀 into this cosmic journey of discovery and let your thoughts soar! 🚀 Don’t just explore, savor the excitement! #BeyondTheOrdinary Your brain will thank you for this exciting journey through the dimensions of awe! 🌍

I have read so many content about the blogger lovers but this paragraph

is truly a nice piece of writing, keep it up.

levoxyl buy online buy synthroid tablets order levoxyl pill

🌌 Wow, this blog is like a rocket soaring into the universe of excitement! 🌌 The thrilling content here is a captivating for the mind, sparking excitement at every turn. 🎢 Whether it’s technology, this blog is a treasure trove of inspiring insights! 🌟 Dive into this exciting adventure of knowledge and let your thoughts soar! 🚀 Don’t just read, savor the thrill! #BeyondTheOrdinary 🚀 will thank you for this thrilling joyride through the realms of awe! 🌍

🌌 Wow, this blog is like a rocket launching into the galaxy of wonder! 🎢 The captivating content here is a rollercoaster ride for the mind, sparking curiosity at every turn. 🌟 Whether it’s lifestyle, this blog is a treasure trove of inspiring insights! #InfinitePossibilities Dive into this exciting adventure of imagination and let your imagination roam! 🚀 Don’t just read, experience the excitement! 🌈 Your brain will thank you for this exciting journey through the realms of discovery! 🌍

prednisolone cheap omnacortil 10mg sale order generic omnacortil 5mg

Pretty nice post. I just stumbled upon your weblog and wished to say that I’ve truly enjoyed

browsing your blog posts. After all I will be subscribing to your feed and I am hoping you write once more soon!

💫 Wow, this blog is like a cosmic journey blasting off into the universe of endless possibilities! 🌌 The thrilling content here is a rollercoaster ride for the imagination, sparking awe at every turn. 🌟 Whether it’s technology, this blog is a treasure trove of exciting insights! #InfinitePossibilities 🚀 into this thrilling experience of discovery and let your mind roam! ✨ Don’t just explore, experience the excitement! #FuelForThought Your mind will be grateful for this thrilling joyride through the worlds of endless wonder! 🚀

💫 Wow, this blog is like a cosmic journey blasting off into the galaxy of excitement! 🌌 The mind-blowing content here is a rollercoaster ride for the imagination, sparking awe at every turn. 🎢 Whether it’s lifestyle, this blog is a goldmine of exciting insights! #MindBlown Embark into this exciting adventure of knowledge and let your imagination roam! 🚀 Don’t just read, savor the excitement! #FuelForThought Your brain will be grateful for this exciting journey through the worlds of discovery! 🚀

serophene ca buy clomiphene generic clomid 100mg us

neurontin without prescription buy neurontin cheap gabapentin 800mg sale

Your writing style is captivating! I was engaged from start to finish.

You have a gift for explaining things in an understandable way. Thank you!

lasix 100mg drug cheap lasix 40mg buy furosemide without prescription

Your ability to distill complex concepts into readable content is admirable.

sildenafil pill brand sildenafil overnight delivery viagra

Your post was a beacon of knowledge. Thank you for illuminating this subject.

Your dedication to quality content is evident. Keep up the great work!

Your post was a beacon of knowledge. Thank you for illuminating this subject.

Your blog is a constant source of inspiration and knowledge. Thank you!

buy vibra-tabs pill monodox cheap doxycycline price

What a compelling read! Your arguments were well-presented and convincing.

rybelsus ca rybelsus 14 mg canada semaglutide 14mg pills

This post is a testament to your expertise and hard work. Thank you!

best online casino for real money blackjack card game real casino online

Your insights have added a lot of value to my understanding. Thanks for sharing.

vardenafil 10mg ca levitra 10mg us vardenafil 10mg ca

Your piece was both informative and thought-provoking. Thanks for the great work!

lyrica 150mg brand order lyrica 75mg online cheap buy pregabalin 75mg pills

zithromax oral suspension

order hydroxychloroquine online plaquenil for sale plaquenil 400mg pill

zithromax for sale

triamcinolone 10mg canada triamcinolone oral buy triamcinolone 4mg generic

tadalafil sale order cialis 20mg pills cialis 10mg

desloratadine 5mg sale purchase clarinex without prescription buy desloratadine tablets

order cenforce 50mg generic cenforce 100mg oral buy cenforce cheap

Your posts always leave me feeling enlightened and inspired. Thank you for sharing your knowledge with us. Asheville sends its love!

Your blog is a true masterpiece, crafted with care and passion. Sending love from Asheville!

Your words have the power to uplift and inspire. Thank you for sharing your gift with us. Asheville loves your blog!

purchase loratadine sale how to buy claritin claritin 10mg for sale

metformin 1000 mg twice daily

Your posts always leave me feeling enlightened and inspired. Thank you for sharing your knowledge with us. Asheville sends its love!

where to buy chloroquine without a prescription where to buy aralen without a prescription aralen price

brand dapoxetine buy cytotec no prescription cytotec order online

metformin er side effects

Your blog is a treasure chest of wisdom and insight. We’re grateful to be readers from Asheville!

glucophage cost metformin 500mg cheap glycomet 1000mg oral

Your blog is a true reflection of your passion and expertise. Asheville is lucky to have you!

purchase xenical generic diltiazem price order diltiazem 180mg online cheap

flagyl without a prescription

Your writing has a way of touching hearts and minds. We’re proud supporters of your blog from Asheville!

Your blog is a treasure chest of wisdom and insight. We’re grateful to be readers from Asheville!

lisinopril drug

furosemide 3169

Thank you for being a beacon of knowledge and inspiration through your blog. Asheville appreciates you!

how long after flagyl can you drink alcohol

does zoloft work right away

zoloft reviews for depression

Your writing is like a gentle breeze, refreshing and uplifting. We’re big fans of your blog from Asheville!

Your blog is a true masterpiece, crafted with care and passion. We’re proud supporters from Asheville!

lisinopril side effect

is salix the same as furosemide

buy norvasc for sale buy generic amlodipine buy norvasc medication

cheap acyclovir zyloprim ca order zyloprim 100mg online

zithromax pediatric

what will gabapentin test positive for

does lasix increase bun and creatinine

Your writing always inspires and educates. Thank you for the effort you put into your blog. Asheville sends its love!

buy rosuvastatin 10mg buy generic crestor buy zetia 10mg for sale

purchase lisinopril pill order zestril 5mg for sale zestril 10mg brand

Your words have the power to uplift and inspire. Thank you for sharing your gift with us. Asheville loves your blog!

glucophage fda

zithromax during pregnancy

glucophage poisoning

Thank you for enriching our lives with your wonderful blog. Asheville is blessed to have you!

gabapentin for depression

motilium 10mg price motilium for sale online tetracycline uk

buy prilosec for sale omeprazole uk buy generic omeprazole 20mg

side effects of cephalexin

escitalopram and thc

gabapentin for dogs: dosage

goodrx amoxicillin

amoxicillin over the counter cvs

is escitalopram controlled substance

inderal 10mg without prescription inderal oral buy clopidogrel 75mg without prescription

affordable essay writing buy essay online uk academic writing uk

will bactrim treat a sinus infection

Marvelous, impressive

Super, fantastic

how long does it take for cephalexin to work

methotrexate 5mg drug methotrexate 2.5mg canada coumadin 2mg canada

Hi there, all is going perfectly here and ofcourse every one is sharing facts, that’s in fact good, keep up writing.

order mobic 15mg without prescription purchase celebrex without prescription buy celecoxib

order generic metoclopramide buy metoclopramide 10mg sale where to buy cozaar without a prescription

can i take 1000 mg of amoxicillin at once

linetogel

Generally I do not read post on blogs, but I wish to say that

this write-up very forced me to try and do it! Your writing taste has been surprised me.

Thank you, very great post.

linetogel

side effects from bactrim

escitalopram pregnancy category

nice content!nice history!! boba 😀

tamsulosin 0.4mg without prescription purchase celebrex generic buy celebrex 200mg pills

wow, amazing

does gabapentin cause hair loss

nice content!nice history!! boba 😀

Excellent effort

nice content!nice history!! boba 😀

escitalopram maximum dose

wow, amazing

wow, amazing

nice content!nice history!! boba 😀

nice content!nice history!! boba 😀

can you overdose on gabapentin

order generic esomeprazole 40mg order generic topiramate 100mg order generic topamax 200mg

Your article helped me a lot, is there any more related content? Thanks!

wow, amazing

zofran 8mg pill buy aldactone 25mg sale aldactone 25mg pill

order sumatriptan 50mg online cheap sumatriptan 25mg ca levaquin price

oral zocor 20mg valacyclovir order valtrex pills

ddavp medication uses

avodart over the counter order generic zantac ranitidine canada

citalopram engorda o adelgaza

depakote sexual side effects

dosage of ddavp nasal spray

cozaar runner

order proscar 5mg online cheap finpecia us fluconazole 100mg brand

buy generic acillin over the counter purchase penicillin generic amoxil cheap

cozaar feet swelling

This is one of the most comprehensive articles I’ve enjoy reading on this topic. Kudos!

citalopram diarrhea

nice content!nice history!! boba 😀

depakote er 500mg

wow, amazing

Terpercaya

danatoto alternatif link!

cipro ca – order bactrim order augmentin generic

cost ciprofloxacin – amoxiclav cheap how to buy clavulanate

Your post has been incredibly helpful. Thank you for the guidance!

This article is a perfect blend of informative and entertaining. Well done!

Your passion for this subject shines through your words. Inspiring!

This blog is a treasure trove of knowledge. Thank you for your contributions!

Your dedication to quality content is evident. Keep up the great work!

Your writing style is captivating! I was engaged from start to finish.

signs of ddavp overdose

depakote toxicity symptoms

Fully resonate with the sentiments shared above – this post is a gem!

alcohol and citalopram

Your post has been incredibly helpful. Thank you for the guidance!

Your creativity and intelligence shine through this post. Amazing job!

Thank you for adding value to the conversation with your insights.

cozaar 50

Such a well-researched piece! It’s evident how much effort you’ve put in.

Your attention to detail is remarkable. I appreciate the thoroughness of your post.

ddavp panhypopituitarism

Thank you for consistently producing such high-quality content.

where is cozaar manufactured

wow, amazing

nice content!nice history!! boba 😀

what is depakote used to treat

order metronidazole 400mg online cheap – cleocin 150mg uk buy zithromax 500mg generic

buy ciplox 500 mg – order doryx online buy erythromycin pills for sale

wow, amazing

This was a great enjoy reading—thought-provoking and informative. Thank you!

is diltiazem a calcium channel blocker

is ezetimibe safe

cost valacyclovir – buy zovirax 800mg sale zovirax generic

diltiazem for cats

augmentin for bronchitis

nice content!nice history!! boba 😀

wow, amazing

buy ivermectin usa – sumycin 250mg price tetracycline 500mg usa

diclofenac forte

nice content!nice history!! boba 😀

Thanks in favor of sharing such a nice idea, post is nice, thats why

i have read it entirely

ezetimibe degradation impurities

contrave dosage for weight loss

effexor side effects sexually

buy flagyl 400mg online – cefaclor 250mg pills buy zithromax 250mg online cheap

contrave alternatives

flomax patent expiration date

nice content!nice history!! boba 😀

buy ampicillin antibiotic buy monodox generic where can i buy amoxil

wow, amazing

Asking questions are in fact nice thing if you are not understanding something completely,

but this article offers fastidious understanding even.

norflex vs flexeril

anacin aspirin

aripiprazole 10mg tab

allopurinol and kidney function

buy furosemide generic diuretic – lasix 100mg ca captopril 25 mg brand

I appreciate the unique viewpoints you bring to your writing. Very insightful!

amitriptyline anxiety

aspirin tylenol

Your post is a ray of light in the darkness. Thank you for brightening my day in a unique way. Keep shining!

Amazing how this content managed to brighten even the cloudiest day. Keep shining with your inspiring posts!

awesome morning commencing with a superb read 📘🌞

amitriptyline for migraines dosage

nice content!nice history!! boba 😀

nice content!nice history!! boba 😀

outstanding sunrise starting with a superb read 📚🌞

excellent sunrise commencing with an incredible literature 🌄📰

aripiprazole erectile dysfunction

can i stop taking allopurinol

incredible morning starting with an outstanding reading 📖🌅

buy glucophage generic – order ciprofloxacin 1000mg sale purchase lincocin pill

augmentin 1000 mg

wow, amazing

wow, amazing

baclofen reviews

buy generic retrovir online – order epivir online cheap allopurinol uk

celebrex cost walmart

bupropion coupon

bupropion while pregnant

celebrex recall

baclofen schedule

buy clozapine pills for sale – buy coversyl no prescription buy famotidine sale

Your thoughtful analysis has really made me think. Thanks for the great enjoy reading!

celecoxib headache

nice content!nice history!! boba 😀

nice content!nice history!! boba 😀

where to buy seroquel without a prescription – effexor usa eskalith pill

buspirone and ciprofloxacin

is celexa an ssri

buspirone recommended dosage

wow, amazing

wow, amazing

hello

hello

wow, amazing

hello

ashwagandha root side effects

can you get high off celecoxib

anafranil 50mg us – sinequan 25mg price sinequan canada

This blog is a treasure trove of knowledge. Thank you for your contributions!

hydroxyzine 25mg pills – endep 25mg drug order endep 25mg for sale

Your insights have added a lot of value to my understanding. Thanks for sharing.

nice content!nice history!! boba 😀

wow, amazing

nice content!nice history!! boba 😀

wow, amazing

nice content!nice history!! boba 😀

nice content!nice history!! boba 😀

amoxicillin online buy – buy keflex pill cipro price

phising

amoxiclav cost – bactrim 480mg ca brand cipro 500mg

lost money

I’m bookmarking this for future reference. Your advice is spot on!

actos play

Your piece was both informative and thought-provoking. Thanks for the great work!

40 units of semaglutide is how many mg

lost money

phising

acarbose impurity

abilify while pregnant

can you drink on abilify

lost money

phising

phising

scam

lost money

phising

phising

lost money

actos attorney

semaglutide online prescription

lost money

scam

lost money

lost money

lost money

protonix dosage 80 mg

scam

phising

is robaxin

remeron and pregnancy

order cleocin online cheap – buy chloromycetin sale order chloramphenicol pill

scam

protonix max dose

repaglinide versus nateglinide monotherapy

repaglinide erstattung

zithromax 250mg generic – purchase flagyl generic ciprofloxacin 500 mg us

I’m amazed by the depth and b enjoy readingth of your knowledge. Thanks for sharing!

Thank you for adding value to the conversation with your insights.

remeron cost

does robaxin cause weight gain

You’ve articulated your points with such finesse. Truly a pleasure to enjoy reading.

Your passion for this subject shines through your words. Inspiring!

I’m amazed by the depth and b enjoy readingth of your knowledge. Thanks for sharing!

Thank you for the hard work you put into this post. It’s much appreciated!

Thank you for adding value to the conversation with your insights.

A masterpiece of writing! You’ve covered all bases with elegance.

I strongly recommend to avoid this site. My personal experience with it has been purely disappointment along with doubts about scamming practices. Be extremely cautious, or even better, seek out a more reputable platform to fulfill your requirements.

I strongly recommend stay away from this platform. The experience I had with it was purely dismay along with doubts about scamming practices. Proceed with extreme caution, or alternatively, seek out a more reputable service to fulfill your requirements.

This post is a testament to The expertise and hard work. Thank you!

ivermectin without prescription – how to get eryc without a prescription order cefaclor pill

The unique perspective is as intriguing as a mystery novel. Can’t wait to read the next chapter.

order albuterol 2mg – order fexofenadine 120mg for sale buy theophylline 400mg generic

I urge you stay away from this platform. My personal experience with it was only dismay along with suspicion of scamming practices. Proceed with extreme caution, or better yet, find a trustworthy site for your needs.

I urge you steer clear of this site. My personal experience with it was purely frustration and concerns regarding deceptive behavior. Proceed with extreme caution, or alternatively, seek out an honest platform for your needs.

I strongly recommend stay away from this site. My own encounter with it was purely disappointment along with doubts about scamming practices. Exercise extreme caution, or better yet, find a trustworthy platform for your needs.

I highly advise to avoid this site. My own encounter with it was purely disappointment as well as concerns regarding deceptive behavior. Exercise extreme caution, or even better, find an honest platform to fulfill your requirements.